Back to Platform Overview

Manage & Bill on Annuities with Avenew.

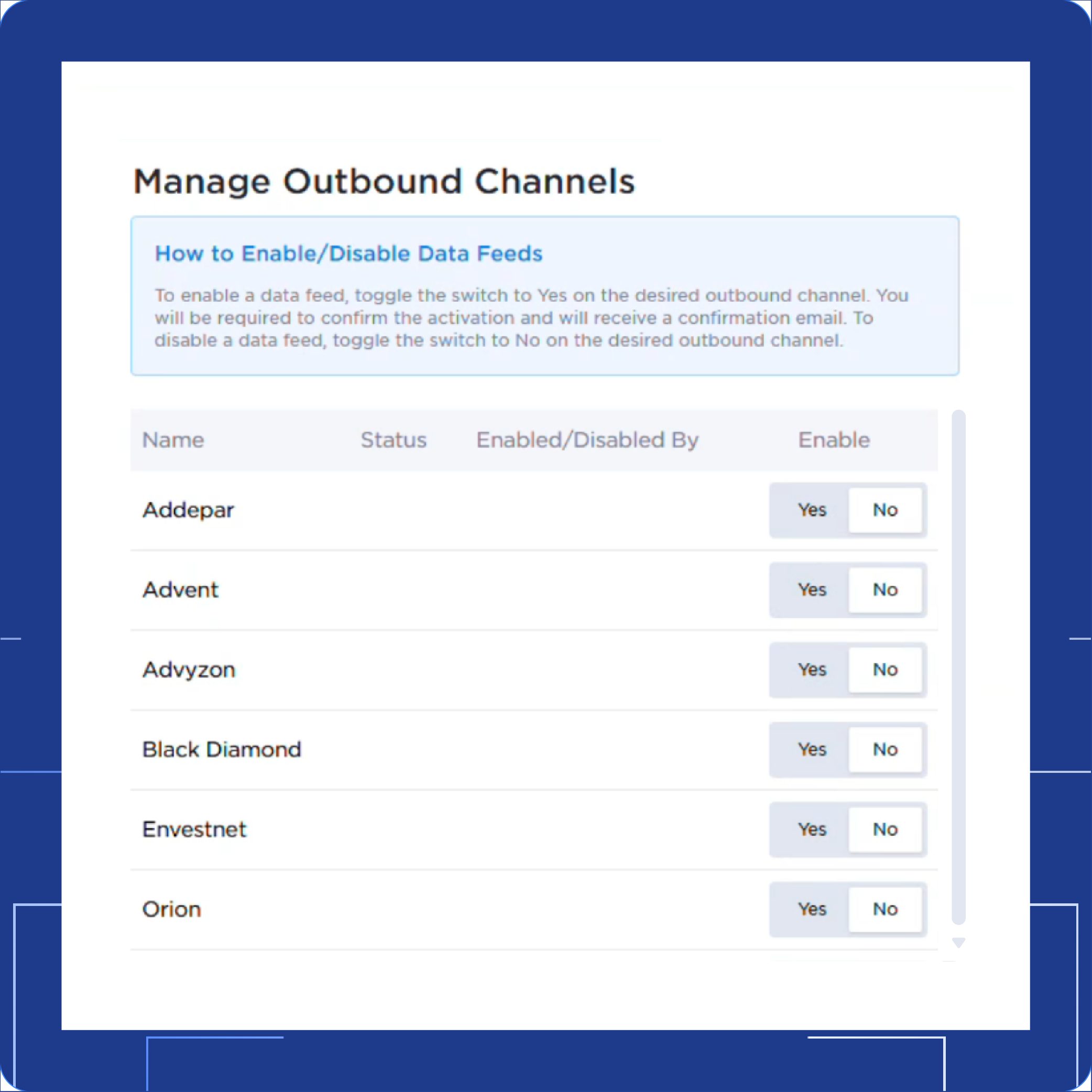

Manage fee-based annuities alongside other investments in clients' portfolios.

No items found.

Why Firms Join DPL

Improve outcomes, elevate your clients’ experience, and grow your business with fee-based annuity and insurance solutions.

Get news and insights straight to your inbox.