Protected Growth Guide

Retirement Realities and Your Portfolio

Investing in the market can be a great way to build wealth for retirement. While riskier than some other investments like bonds, equities can potentially earn higher returns and outpace inflation, helping grow your nest egg over the long term.

As retirement approaches, however, your advisor may recommend shifting some of your equity portfolio to safer options that offer protection from market volatility.

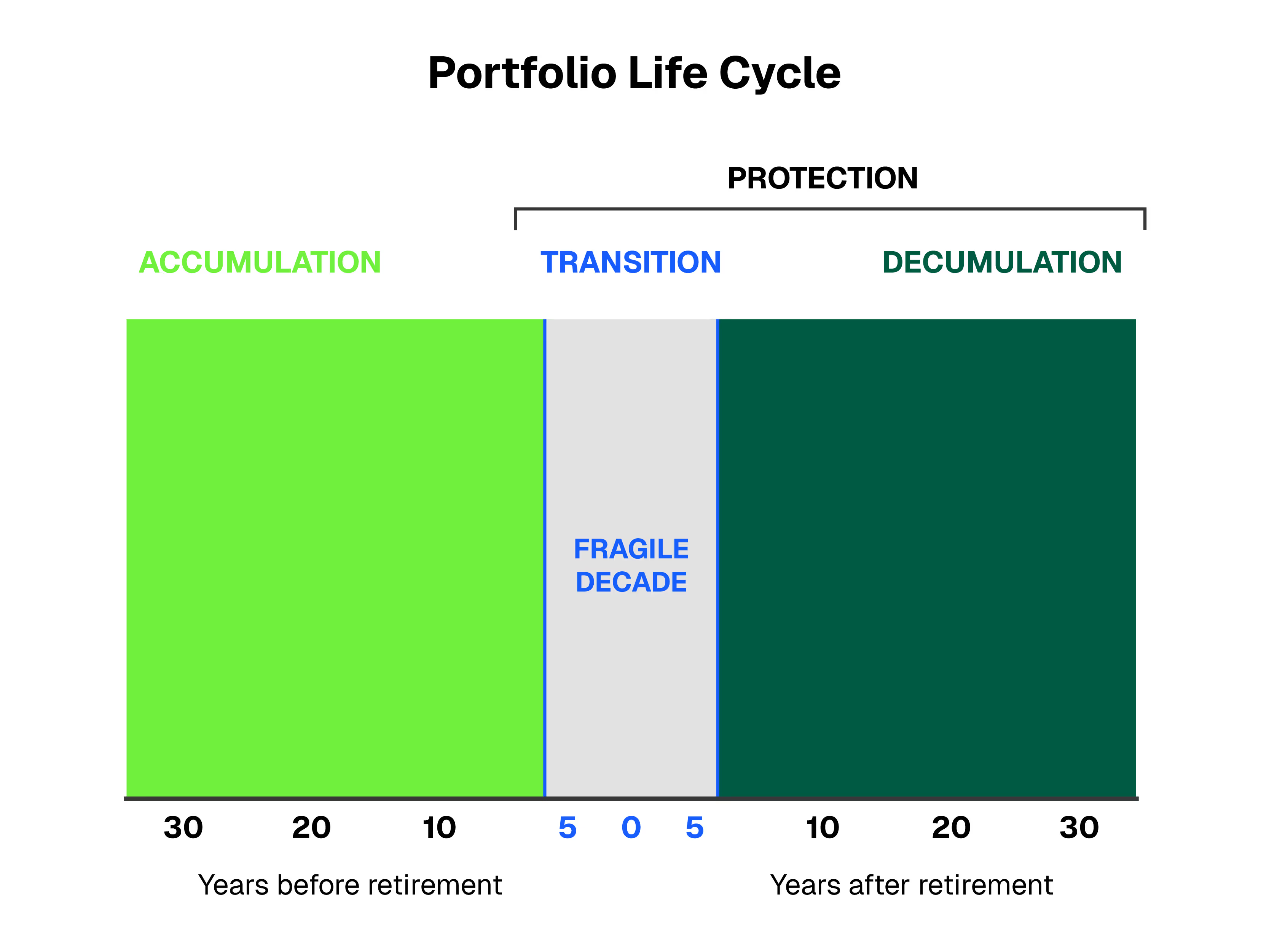

Adding protection can be important because significant market losses during the 5 years before and 5 years after retirement, referred to as “The Fragile Decade,” can deplete a portfolio to the point it can no longer generate sufficient retirement income.

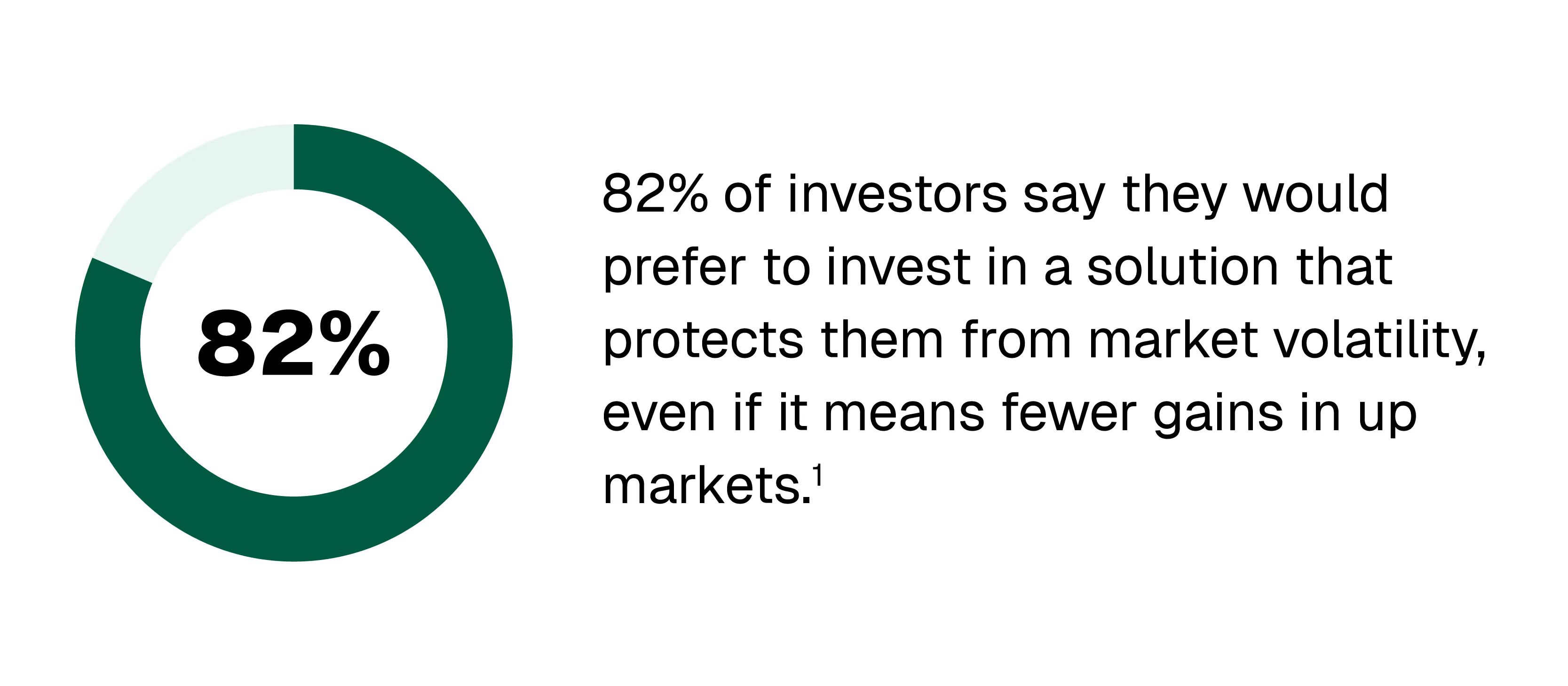

If you’re a conservative investor, protecting your money from market losses as you near retirement is likely a welcomed strategy. If you’re less risk averse, you may not want to sacrifice potential market gains, even if it’s prudent to de-risk your portfolio from large equity allocations and potential losses.

Today, options are available that provide a range of choices and flexibility to customize levels of protection and growth potential that are right for your goals and needs.

How to Think About Protection in Your Portfolio

There are many reasons why it may make sense to add protection to your portfolio:

Income: You’re depending on your investment portfolio to generate retirement income and can’t risk a significant market downturn

Peace of Mind: Concern about market volatility is making it hard to stick with your financial plan and stay invested when things get choppy

Risk: You have high equity exposure in your portfolio and, while you fear losses, you also fear missing out on potential gains

If you’re invested in the market and are nearing or in retirement, it’s important to be prepared for the inevitable ups and downs, and have confidence that your plan meets both your financial and psychological needs.

Work with your advisor to determine your goals, needs, and timeline, as well as your comfort with risk and loss potential. Then consider your options.

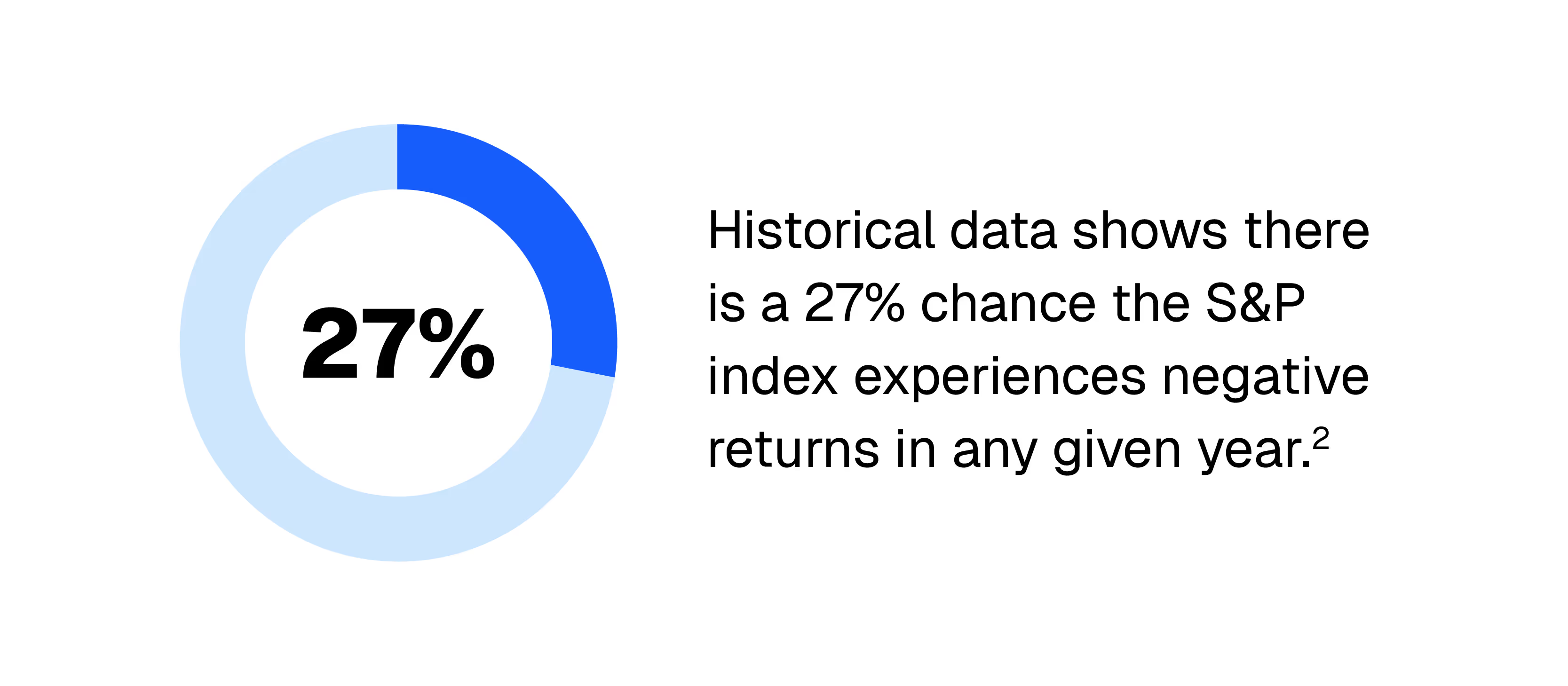

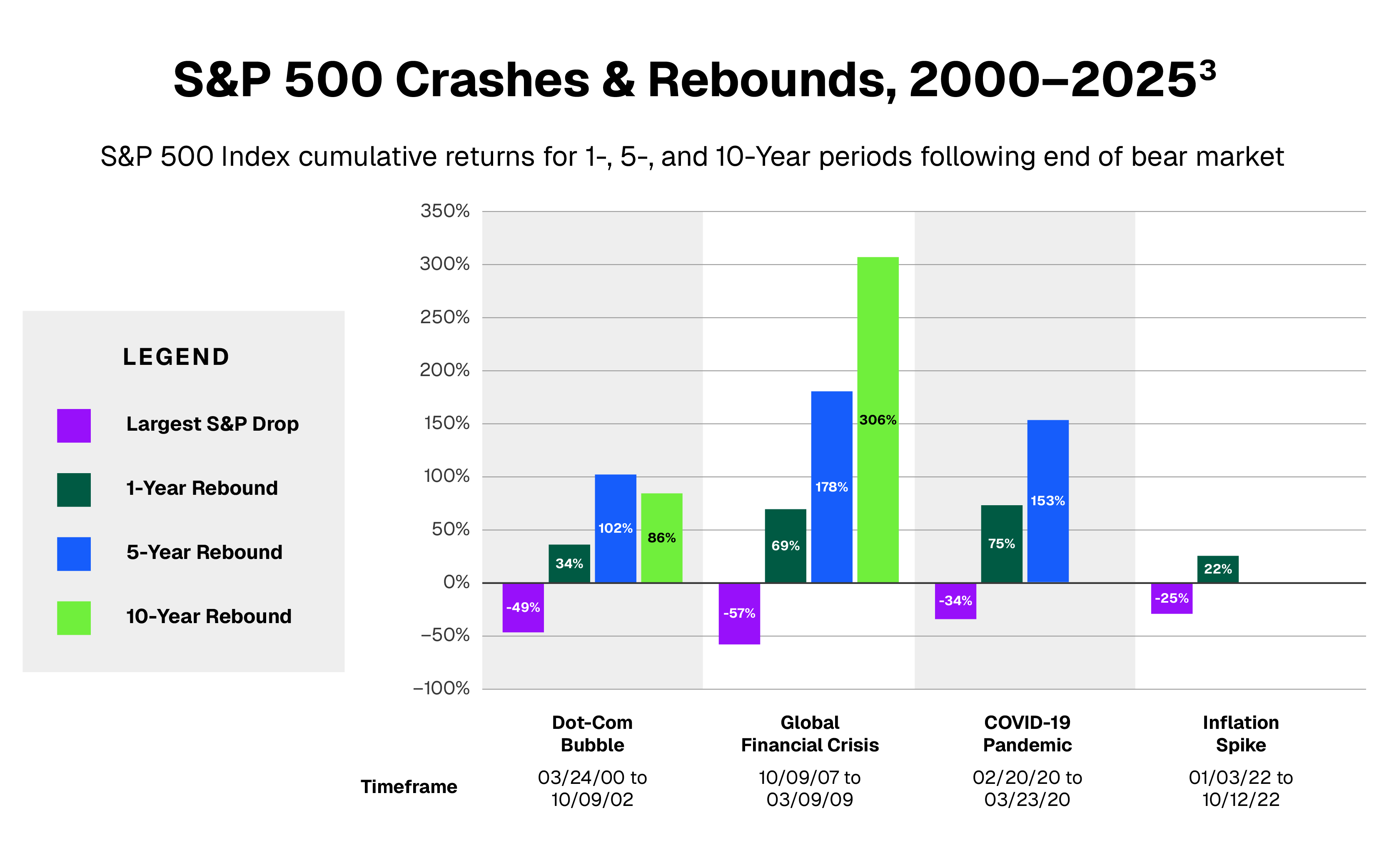

The S&P 500’s shocks and subsequent cumulative returns demonstrate the market’s inevitable volatility. Historically, gains have followed declines, so staying invested through volatility can make sense if your retirement timeline allows for your portfolio to recover before you begin taking income withdrawals. If you experience significant portfolio losses just before or soon after you retire, you risk running out of money during retirement.

Modern Annuities Offer a Range of Protection Options

Annuities can be a smart option to add protection to your portfolio. A range of product types is available from leading insurance carriers, designed to provide complete or partial principal protection, protected growth, and guaranteed lifetime income for retirement.

Today’s modern annuities are lower-cost and often provide better benefits than traditional, commission-free products. “Commission-free,” or “no-load,” annuities are built without sales commissions, enabling your fiduciary advisor to use them in your financial plan to provide protected growth and guaranteed income solutions customized for your specific wants and needs.

“It now is possible to frame an annuity, or the protections it provides, as an asset class for households to help manage market risks and the risk of outliving assets (in retirement).”

— Wade Pfau, PhD | Professor of Retirement Income at The American College of Financial Services

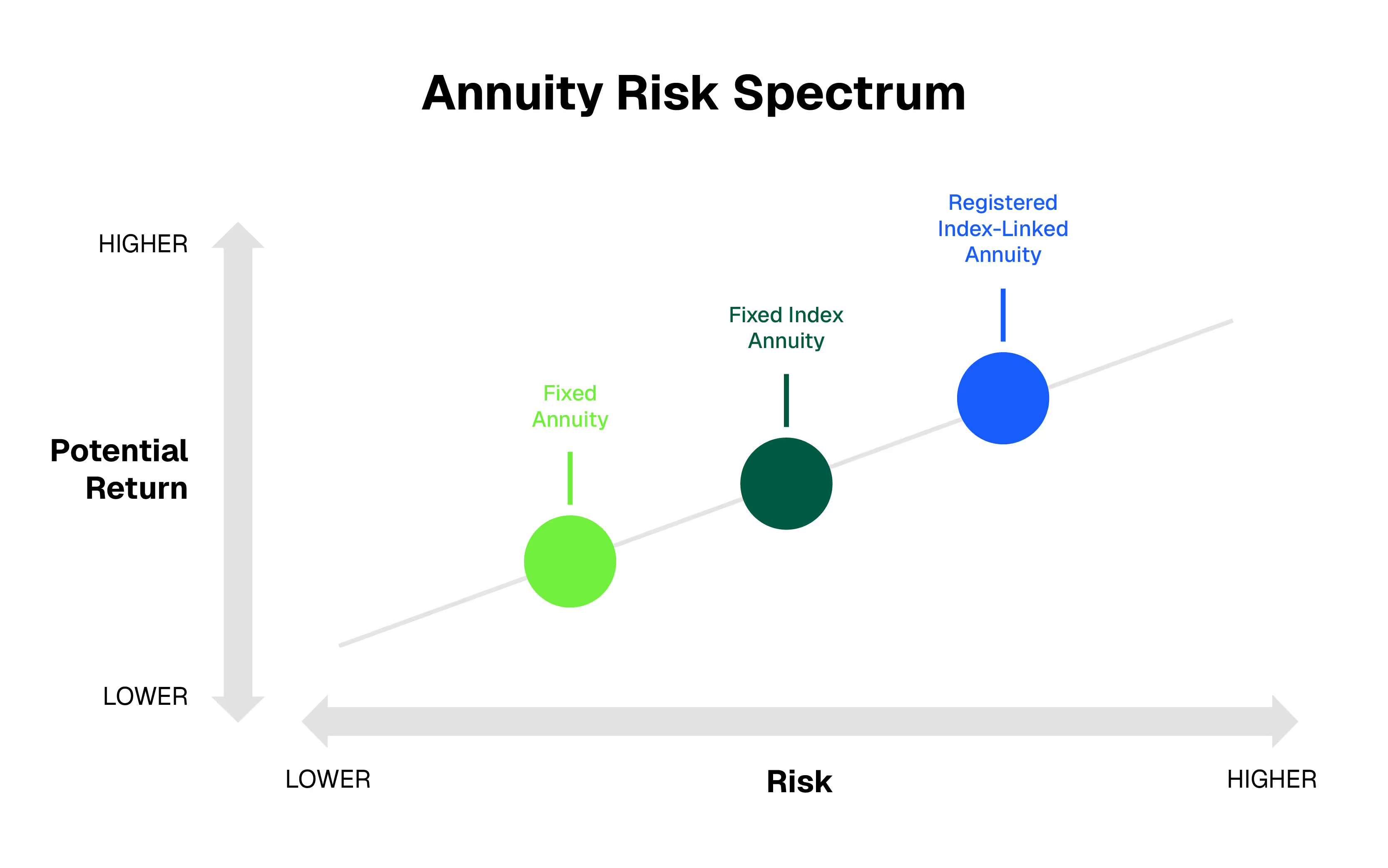

Complete Protection with a Fixed Rate of Return: Multi-Year Guaranteed Annuity (or “MYGA”)

Investor Risk Profile: Low

Protection Level Provided: High

Key Benefits: Complete principal protection with a guaranteed rate of return for a specific period of time; often higher returns than CDs or money market funds; assets grow tax deferred; multiple products available commission-free

Typical Funding Sources: Cash (Savings), CDs, Fixed Income

Multi-Year Guaranteed Annuities (MYGAs) are a type of fixed annuity. These simple, CD-like products have been very popular in the last several years because they offer often higher rates of return than CDs and a range of terms from 2 to 10 years.

Consider a MYGA when you’re looking for:

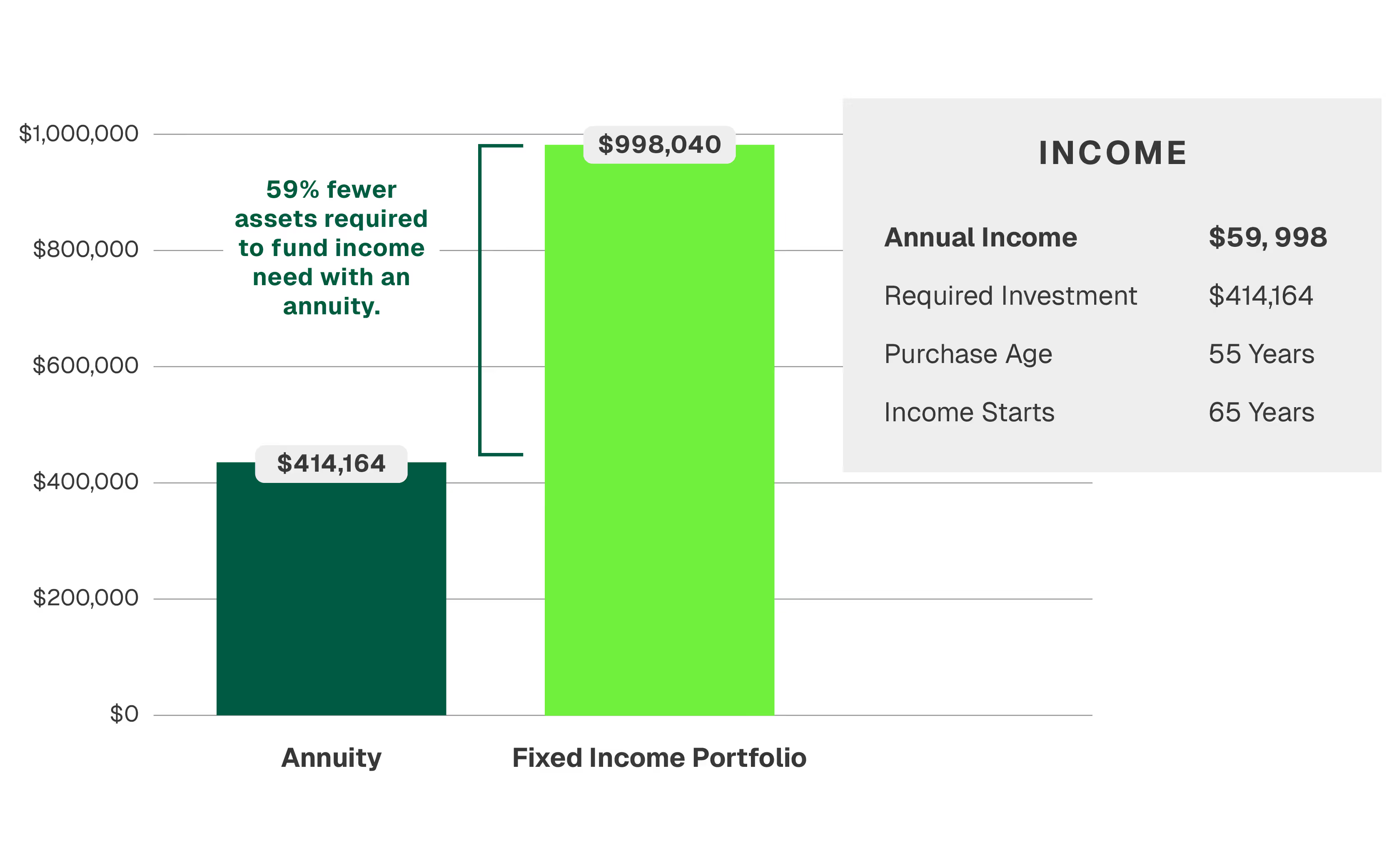

Principal Protection: MYGAs offer complete principal protection and a guaranteed rate of return. These simple products often are used to protect and grow assets tax deferred when nearing or in retirement.

Fixed Income Alternative: A good solution to de-risk your portfolio from equities and secure a consistent stream of income.

Cash Replacement: A high-yielding option for cash or cash investments like CDs or money market funds to help improve returns (subject to the terms of the contract).

Protected Growth with Complete Downside Protection: Fixed Index Annuity (FIAs)

Investor Risk Profile: Conservative (Often used by investors whose risk profile has become more conservative)

Protection Level Provided: High

Key Benefits: Total downside protection with market-like exposure for growth; ability to generate guaranteed lifetime income; no fees if not purchasing an income benefit; liquidity and flexibility; multiple products available commission-free

Typical Funding Sources: Fixed Income, Money Market

If you’re willing to take a little risk for greater upside, FIAs can potentially capture more return than MYGAs due to market exposure and can potentially outperform fixed income. FIAs offer principal protection, meaning you won’t lose any of the money you put into the product.

Consider a FIA when you’re looking for:

Principal Protection: FIAs provide 100% principal protection and are used when nearing or in retirement to protect assets while providing market-like exposure for growth.

Fixed Income Alternative: Allocating a portion of your fixed income portfolio to an FIA can be an effective strategy to increase returns with a less risky asset. FIAs typically have higher average returns over 10-year periods than bond yields.

Guaranteed Lifetime Income: With the purchase of a “living benefit,” FIAs can be used to generate guaranteed lifetime income.

Customizable Levels of Protection and Growth: Registered Index Linked Annuity (RILA)

Investor Risk Profile: Moderate

Protection Level Provided: Moderate

Key Benefits: The ability to customize levels of downside protection and upside exposure to market indices; often simpler products than structured notes; multiple products available commission-free

Typical Funding Sources: Bond or Equity Allocations, Fixed Income

A Registered Index Linked Annuity, or RILA, is a newer product designed to provide customizable levels of equity market participation and downside protection. RILAs can offer potentially greater upside than a FIA, though the trade-off is accepting a level of downside risk, that you can customize. Investors often purchase RILAs as an equity allocation compliment to capture growth potential while reducing risk in the portfolio.

Consider a RILA when you’re looking for:

Principal Protection: Registered index linked annuities are typically used when nearing retirement to add a level of protection against market losses, while also providing the potential for higher returns due to higher cap rates than other insurance vehicles.

Equity Replacement: RILAs can be a good solution to de-risk your portfolio from large equity allocations while still providing market exposure and the potential for growth.

Bond Replacement: If you have under-performing bonds, RILAs can potentially provide more return with a level of protection, though it’s important to understand the risks involved.

Income: With the purchase of a “living benefit,” registered index linked annuities can be used to generate guaranteed lifetime income with allocation flexibility and liquidity (beyond potential market value adjustments or surrender periods).

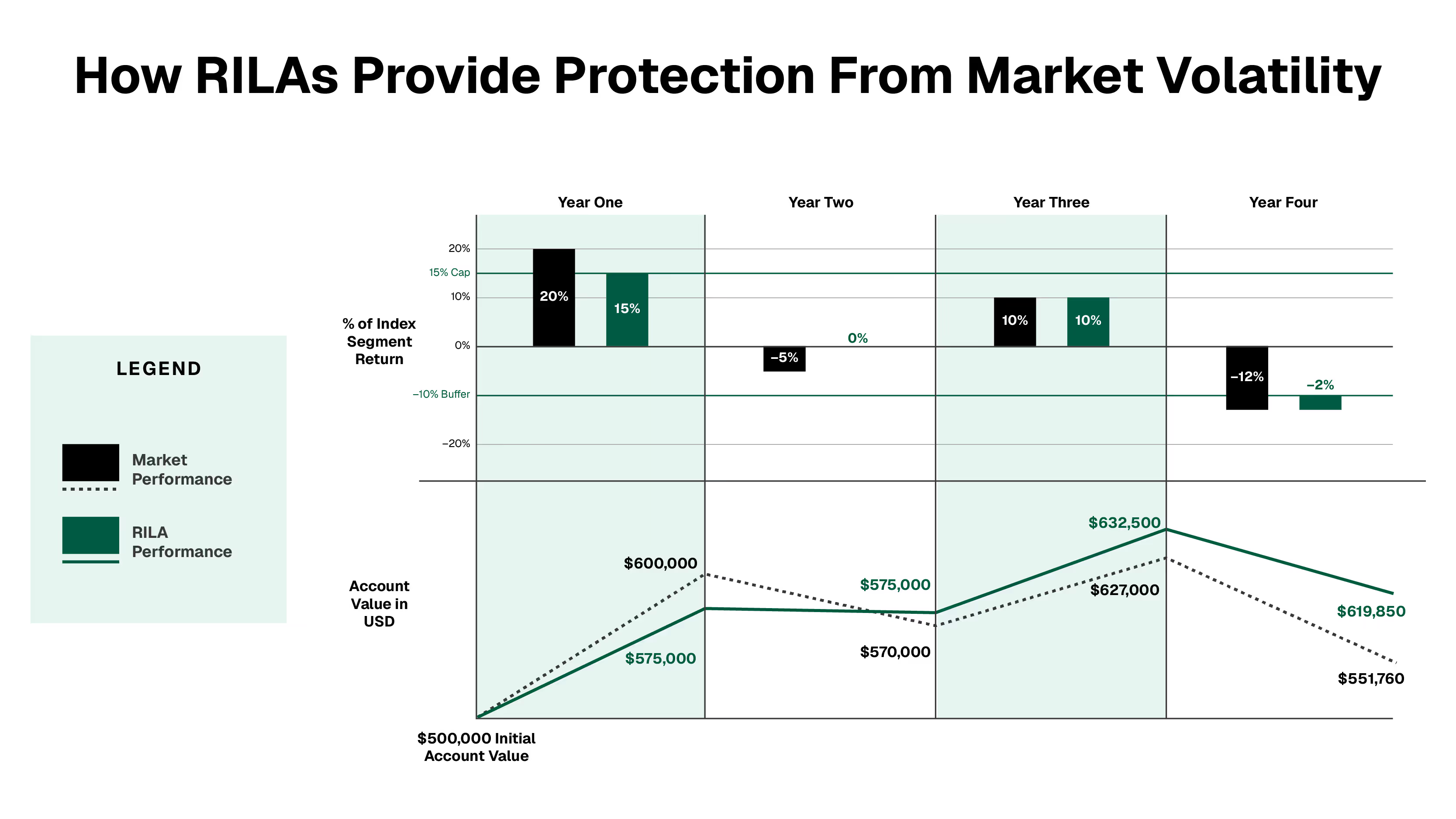

The downside protection of a RILA, commonly referred to as a “buffer,” protects against the first losses in a down market. For example, a 10% buffer would protect you from the first 10% of losses in a negative year, meaning that if the market is down 12%, you are only down 2%. Any losses that fall within the buffer, are absorbed by the insurance company. On the upside in this example (below), market gains are capped at 15% which means you will not realize market returns greater than 15%. RILAs offer a variety of cap and buffer rates to fit your tolerance.

Next Steps

Annuities are powerful tools designed to provide complete or partial principal protection, protected growth, and guaranteed lifetime income for retirement. And, now, modern annuities are available without commissions from many leading insurance carriers, offering lower costs and improved benefits.

There are many types of annuities, and it’s important to work with your financial advisor to determine if an annuity fits into your financial plan and which product is right for you. We can help.

[press-a-contact-location]

Sources:

1 Lincoln Financial

2 Allianz Life, “A Closer Look at Historical Returns”

3 https://www.mfs.com/content/dam/mfs-enterprise/mfscom/sales-tools/sales-ideas/mfse_resdwn_fly.pdf

Disclosures:

Guarantees are based on the claims paying ability of the insurance carrier issuing the product.

• Not a deposit • Not FDIC or NCUSIF insured • Not guaranteed by the institution • Not insured by any federal government agency • May lose value

When evaluating the purchase of a variable annuity, you should be aware that variable annuities are long-term investment vehicles designed for retirement purposes and will fluctuate in value; annuities have limitations; and investing involves market risk, including possible loss of principal.

The general distributor for variable products is Johnstone Brokerage Services ("JBS"), member FINRA/SIPC 117 San Augustine Street, Center TX 75935. JBS is wholly owned by DPL Financial Partners.

Fixed index annuities are not stock market investments and do not directly participate in any equity, bond, other security, or commodities investments. Unless stated otherwise, market Indices do not include dividends paid on the underlying stocks, and therefore do not reflect the total return of the underlying stocks; neither an index nor any market index annuity is comparable to a direct investment in the equity markets. Clients who purchase index annuities are not directly investing in a stock market index.

Fixed indexed annuities are contracts purchased from a life insurance company that are designed for long-term retirement goals. While the interest rate credited to an indexed account is linked to the performance of an underlying index, premium payments made to a fixed index annuity are never directly invested in the stock market.

All guarantees are based on the financial strength and claims-paying ability of the issuing insurance company.

The purchase of an annuity within a retirement plan that already provides tax deferral under sections of the Internal Revenue Code results in no additional tax benefits. An annuity should be used to fund a qualified plan based upon the annuity’s features other than tax deferral. All annuity features, risks, limitations, and costs should be considered prior to recommending the purchase of an annuity within a tax-qualified retirement plan.

Variable products are sold by prospectus. Carefully consider the investment objectives, risks, charges and expenses. The product and underlying fund prospectuses contain this and other important information. Investors should read them carefully before investing.

This material is not a recommendation to buy or sell a financial product or to adopt an investment strategy. Investors should discuss their specific situation with their financial professional.

© 2025 DPL Financial Partners, LLC. All rights reserved.

.avif)